When buying a home, it’s easy to get swept up in the excitement of owning your own space. But lurking behind the dream home and white picket fence is a financial commitment that can quietly erode your wealth over time if not managed carefully. Home loans, often seen as a necessary step in homeownership, can become a “silent killer” of financial health. Here’s why:

The True Cost of Borrowing

Most borrowers focus on the loan’s principal—the amount borrowed to purchase the home. However, over the life of a 20 or 30-year mortgage, the total interest paid can be staggering, often exceeding the original loan amount. For instance, on a $300,000 loan at a 4% interest rate over 30 years, the total interest paid can surpass $215,000. This means you’re paying more than double the price of the home over time.

The Trap of Variable Interest Rates

While fixed-rate mortgages offer stability, variable-rate loans can seem tempting with their initially lower rates. However, as market conditions change, these rates can increase significantly, leading to a sudden spike in monthly payments. For families on a tight budget, this can spell disaster, forcing difficult financial decisions or even leading to foreclosure.

Opportunity Cost: What Are You Sacrificing?

Home loans tie up a significant portion of your finances. The money spent on mortgage payments could potentially be invested elsewhere, like in stocks, education, or starting a business. By locking funds into a long-term loan, homeowners may miss out on opportunities to build wealth in other ways.

The Inflation Illusion

Owning a home is often touted as a hedge against inflation, as property values tend to rise over time. However, the cost of servicing a mortgage—especially if it’s coupled with rising property taxes, insurance, and maintenance costs—can outpace salary increases. This means that even as your home’s value goes up, your financial health may not improve proportionally.

Market Volatility: The Risk of Negative Equity

Housing markets fluctuate. In the event of a downturn, homeowners can find themselves with a property worth less than the remaining mortgage balance—a situation known as negative equity. This not only limits options for refinancing but can also trap families in homes they can’t afford to sell.

The Importance of Financial Discipline

Long-term financial commitments require consistent discipline. Unforeseen events like job loss, health issues, or economic downturns can disrupt income flow, making it difficult to keep up with mortgage payments. Missing payments can lead to penalties, credit score damage, and even the loss of your home.

Tips to Avoid the Silent Killer Trap

1. Understand the Total Cost: Calculate the total interest payable over the life of the loan and see if it aligns with your financial goals.

2. Opt for a Fixed Rate: If possible, choose a fixed-rate mortgage to protect against future rate hikes.

3. Pay Extra When Possible: Paying a little extra each month can significantly reduce the interest paid over time.

4. Build an Emergency Fund: Ensure you have a financial cushion to cover mortgage payments in case of unexpected expenses.

5. Consider Refinancing: Regularly review your mortgage terms and explore refinancing options to secure better rates.

Let’s break down the costs of a 1 crore (10 million) property with an 8% annual interest rate over a 30-year tenure.

Loan Details:

• Principal Amount: ₹1,00,00,000 (1 crore)

• Interest Rate: 8% per annum

• Loan Tenure: 30 years (360 months)

EMI Calculation:

The formula for calculating EMI (Equated Monthly Installment) is:

EMI = {P * r * (1 + r)^n}/ {(1 + r)^n – 1}

Where:

• P = Principal loan amount = ₹1,00,00,000

• r = Monthly interest rate = Annual interest rate / 12 = 8% / 12 = 0.67% = 0.0067

• n = Number of monthly installments = 30 years × 12 = 360

Using this formula, let’s calculate the EMI.

EMI and Total Payment:

– Monthly EMI : ₹73,376

– Total Payment Over 30 Years: ₹2,64,15,525

Breakdown:

1. Total Interest Paid:

Total Payment – Principal = ₹2,64,15,525 – ₹1,00,00,000 = ₹1,64,15,525

2. Summary:

– Over 30 years, you would pay almost 1.64 times the principal amount in interest alone.

– This example highlights the significant cost of long-term loans, making it crucial to consider strategies like prepayment or refinancing to reduce interest burden.

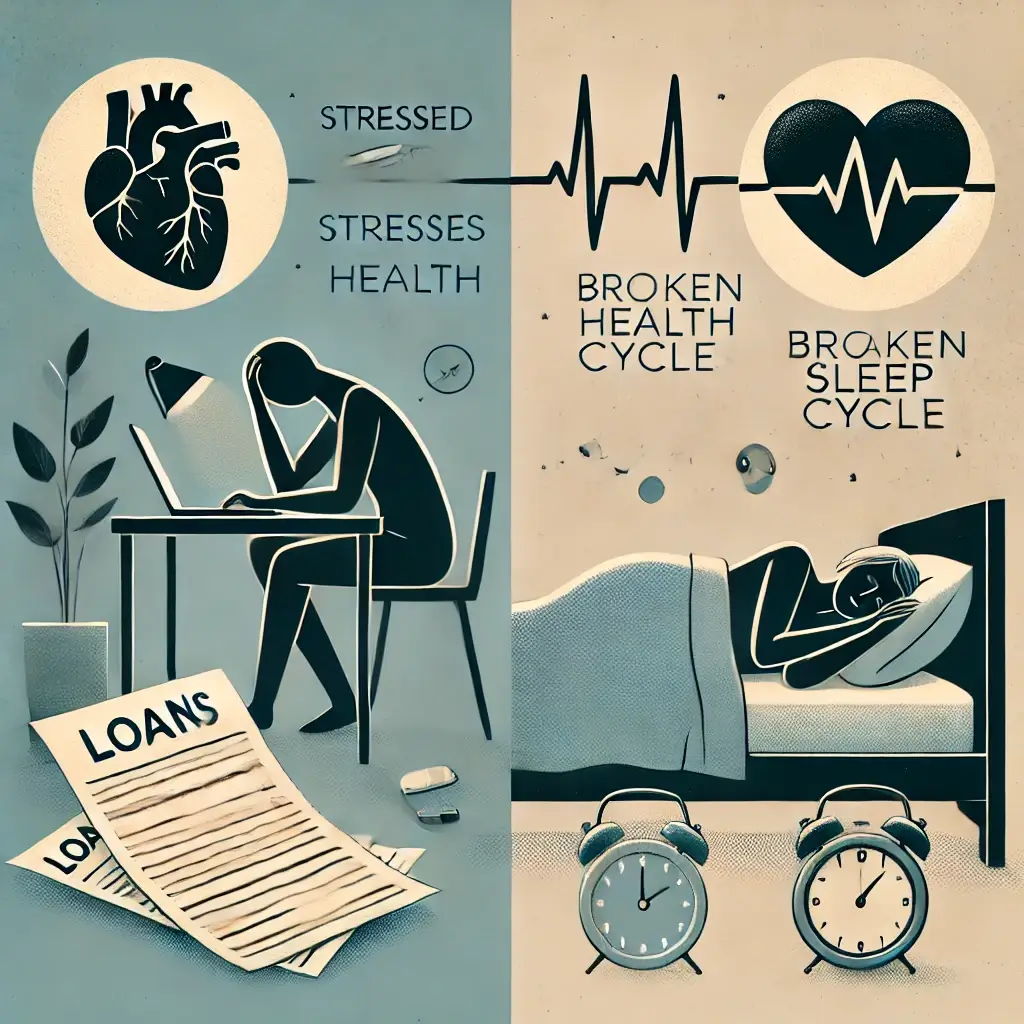

Taking on a loan, especially a long-term one like a home mortgage, can have significant psychological and physical impacts. The pressure to meet financial obligations can affect a person’s mental well-being and overall health. Here’s how:

Psychological Impact

1. Stress and Anxiety:

– The pressure to meet monthly payments can lead to constant worry, especially during times of financial instability. The fear of defaulting on a loan or losing one’s home can cause chronic stress and anxiety.

2. Decision Paralysis:

– Large financial commitments can create a sense of being “trapped,” making people hesitant to make other life decisions, such as changing jobs, relocating, or making additional investments.

3. Depression:

– Persistent financial strain and the feeling of being overwhelmed by debt can contribute to depression. This is often exacerbated if the loan is seen as a burden rather than a tool for achieving a goal.

4. Relationship Strain:

– Money is a common source of conflict in relationships. Disagreements over how to manage loan payments or financial priorities can strain partnerships and family dynamics.

5. Reduced Cognitive Function:

– Financial stress can reduce cognitive capacity, making it harder to focus on other tasks or make rational decisions. This can perpetuate a cycle of poor financial choices, worsening the situation.

Physical Impact

1. Chronic Stress-Related Health Issues:

– Long-term stress due to financial pressure can lead to health problems like hypertension, cardiovascular diseases, and weakened immune systems.

2. Sleep Disorders:

– Anxiety over finances often disrupts sleep patterns, leading to insomnia or poor-quality sleep. This lack of rest can further impact mental health, creating a vicious cycle of stress and fatigue.

3. Poor Lifestyle Choices:

– Under financial strain, people may neglect healthy habits, such as exercising or eating well, due to lack of time, energy, or resources. This can lead to weight gain, poor nutrition, and other health issues.

4. Substance Abuse:

– Some individuals might turn to alcohol, drugs, or other unhealthy coping mechanisms to deal with financial stress, which can lead to addiction and further physical and mental health problems.

5. Impact on Overall Quality of Life:

– The constant need to priorities loan payments over other expenses can lead to a compromised lifestyle. Skimping on healthcare, recreation, or social activities to manage loan payments can diminish overall life satisfaction.

Mitigating the Impact

1. Financial Planning:

– Create a realistic budget that accounts for loan payments and other necessary expenses. This helps manage cash flow and reduces financial surprises.

2. Emergency Fund:

– Maintaining an emergency fund can provide a buffer against unexpected expenses or income disruptions, reducing stress related to loan payments.

3. Professional Support:

– Financial advisors can offer strategies for managing debt, while counselors or therapists can provide support for mental health issues arising from financial stress.

4. Lifestyle Adjustments:

– Adopting stress-reducing practices such as exercise, meditation, and maintaining a support network can help mitigate the physical and psychological effects of financial pressure.

Understanding and addressing the psychological and physical impacts of loans can help individuals manage their financial commitments without compromising their overall well-being.

Conclusion: Owning a Home Without Owning Your Wallet

Homeownership remains a cornerstone of the Dream, but it’s essential to go into it with eyes wide open. By understanding the true costs and potential pitfalls of home loans, you can avoid letting this “silent killer” slowly drain your finances. With the right strategies and financial discipline, you can turn your home into an asset, rather than a liability.

Post Disclaimer

Disclaimer

1. The Alpha Wealth is a wealth advisory offering financial services viz and third-party wealth management products. The details mentioned in the respective product/ service document shall prevail in case of any inconsistency with respect to the information referring to BFL products and services on this page.

2. All other information, such as, the images, facts, statistics etc. (“information”) that are in addition to the details mentioned in the The Alpha Wealth product/ service document and which are being displayed on this page only depicts the summary of the information sourced from the public domain. The said information is neither owned by The Alpha Wealth nor it is to the exclusive knowledge of The Alpha Wealth. There may be inadvertent inaccuracies or typographical errors or delays in updating the said information. Hence, users are advised to independently exercise diligence by verifying complete information, including by consulting experts, if any. Users shall be the sole owner of the decision taken, if any, about suitability of the same.

Standard Disclaimer

Investments in the securities market are subject to market risk, read all related documents carefully before investing.

Research Disclaimer

Sub-Broking services offered by Sharekhan LTD | REG OFFICE: Badlapur, Thane 421503. Corp. Office: ---, Maharashtra 421503. SEBI Registration No.: --| BSE Cash/F&O/CDS (Member ID:--) | NSE Cash/F&O/CDS (Member ID: --) | DP registration No: --- | CDSL DP No.: --| NSDL DP No. --| AMFI Registration No.: ARN –253455.

Website: https://thegreenbackboogie.com//

Research Services are offered by The Alpha Wealth as Research Analyst under awaiting SEBI Registration No.: ---.

Details of Compliance Officer: -- | Email: --/ --- | Contact No.: -- |

This content is for educational purpose only.

Investment in the securities involves risks, investor should consult his own advisors/consultant to determine the merits and risks of investment.

hi